Financial Capital – Last Line of Defense

the importance of optimizing financial capital for retirement by matching investments to anticipated spending needs, ensuring a stable financial foundation while exposing excess capital to higher-risk investments for growth.

As a reminder, there are 3 sources of capital – Human, Financial and Social. Today, we are going to expand on Financial Capital, and discuss why this is your last line of defense.

But first, some definitions:

Retirement: The process of executing your pre-defined financial independence.

Financial Independence: Placing no reliance on a job or anyone else to maintain your chosen lifestyle.

Financial Capital: Money that is held within investments. Examples are as follows:

- 401(k)

- 403(b)

- IRA

- Roth IRA

- Taxable Brokerage Accounts

- Checking/Savings

- Rental Real Estate - note the illiquidity of the hard asset of real estate poses an issue to navigate in any retirement plan.

Last Man Standing:

Financial capital is your last man standing within your retirement financial structure. Social security and human capital are fabulous resources for retirement spending, but any overages over those two buckets must come from your financial capital. The question most households ask regarding financial capital is: “Am I appropriately invested?”

To answer this question, let’s walk through a previous scenario we posed within the blog titled “Sources of Capital.”

Scenario:

4 foundational numbers that are critical to know for any retirement plan construction are as follows:

- Annual Lifestyle Spending Number

- Annual Social Security Income for Both Spouses: Social Capital

- Annual Part-Time or Employment Income: Human Capital

- Annual Financial Capital Required to Fund Lifestyle: Financial Capital

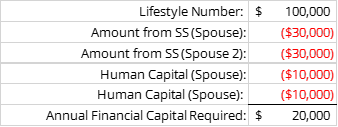

For example, if you’ve determined your annual lifestyle spending number to be $100,000, let’s assume both you and your spouse in retirement will receive $30,000 each of social security benefits (social capital) and you both plan to work somewhere that you desire to work part-time (human capital) and earn $10,000 each. (I like to give the example, ‘if you like tools, you can go work with tools at Home Depot’). The question then becomes – to maintain this lifestyle – what do I need annually from my financial capital? The answer is not $100,000 – it is $20,000.

This analysis above is a simple yet powerful way to understand how to maximize your financial capital through retirement. An almost bulletproof strategy to give confidence that you can spend $100,000 throughout retirement is to invest your annual required financial capital in a bond or fixed income portfolio that matches the timing of when you will spend those funds. The technical term for this is a matched-duration immunized portfolio.

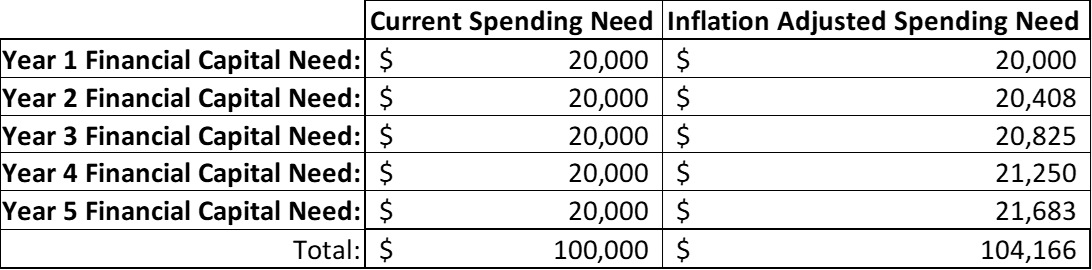

There are a lot of words there that are better explained with a visual, in my opinion. You protect your annual required financial capital need by investing in low risk, inflation protected investments to give you the highest probability of not outliving your money. Assuming you only needed to invest $20,000 for 5 years for retirement (for simplicities sake), see below visual:

Now – if we protect the inflation adjusted number of $104,166 for the next 5 years of spending, the question then becomes:

“What do we do with the rest of my investments?”

Traditional practice is to move the majority of a retiree’s assets into more fixed income to preserve wealth. In theory, this absolutely makes sense. However, what this method blatantly shows is a lack of expertise in financial planning and portfolio construction.

Back to our original question of what you should do with the rest of your investments. Once we have the $104,166 protected, I can then expose the rest of my portfolio to investments with higher expected returns, assuming there are no other planned expenditures over the next 5-year period. If my total financial capital is $500,000, I can in theory expose $400,000 to stock ownership.

However, if I only have $150,000 of financial capital, I should only expose $50,000 of my investments to stock ownership.

What this investment framework gives a household is clarity and confidence – you are protected where you need to be protected, and you are growing your wealth where you can take appropriate risk. We call this technique building your financial floor, and exposing the rest to upside.

Free Resource:

Download Josh's Balance Sheet Template

Want to get started putting Josh’s suggestions into practice? Join the AWM Network through the form below and receive a free Balance Sheet & Income Statement Template.

SIGN ME UP

Conclusion:

Do not fall prey to a traditional money manager that states that you need to reduce risk in your portfolio without proper analysis done on your individual situation. Financial mass marketing is rampant, and everyone’s situation requires true expertise and a good amount of listening.

Your financial capital should be optimized based on your expected lifestyle cash outflows. Only then can you have clarity and confidence that you are invested appropriately for retirement.

Transcript

Share this post

Related articles

Your Family Office

We're here to help you navigate.

Our advisors are ready to serve as your Athlete Family Office.

Your Family Office

We're here to help you navigate.

Our advisors are ready to serve as your Athlete Family Office.